Our Leadership Team

Our Leadership Team

Find An Advisor

Find An Advisor

Our Platform

Our Platform

Advisory

Advisory

Alternatives

Alternatives

Insurance

Insurance

Specialized Services

Specialized Services

Individual Investors

Individual Investors

Retirees

Retirees

Business Owners

Business Owners

Family Offices & Institutions

Family Offices & Institutions

Doctors

Doctors

Tenants

Tenants

Accountants

Accountants

RIA / Advisor Firms

RIA / Advisor Firms

News | Retirement Planning | Wealthy Behaviors

New 401(k) and IRA Limits Could Equal an Additional 300k in Your Pocket

Posted on January 10, 2023

How’s an additional $313,532 sound to you? Sorry, were getting ahead of ourselves…

In November of 2022, the IRS announced a number of changes coming in 2023. Among those changes were new IRA and 401(k) maximum contribution limits. (See the full article linked here, that includes additional details and other important changes to discuss with your advisor.)

Highlights

- The contribution limit for employees who participate in 401(k), 403(b), most 457 plans, and the federal government’s Thrift Savings Plan is increased to $22,500, up from $20,500.

- The limit on annual contributions to an IRA increased to $6,500, up from $6,000.

- The catch-up contribution limit for employees aged 50 and over who participate in 401(k), 403(b), most 457 plans, and the federal government’s Thrift Savings Plan is increased to $7,500, up from $6,500.

This is a direct reaction to recent increases in inflation. The increase of $22,500 from $20,500 is a 10% adjustment. We are suggesting that clients increase their savings 10% to all retirement accounts. Let your advisor know if you’d like your retirement savings to increase 10% to match inflation.

So, what do I do with that information?

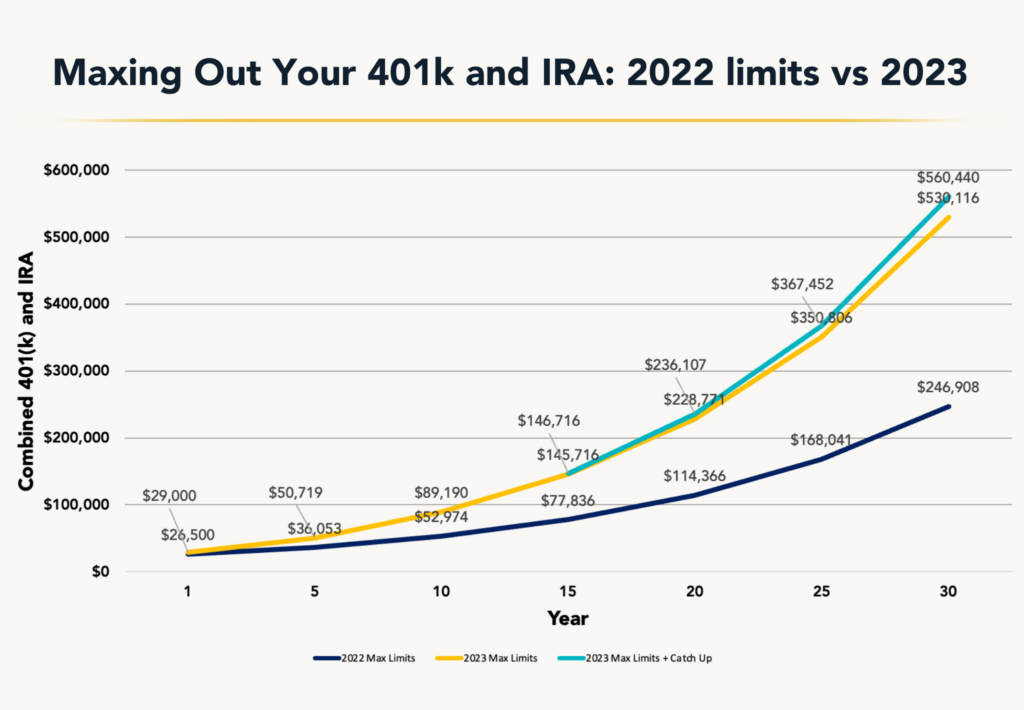

In total, if you were to max out both your IRA and 401(k), you would be investing an additional $2,500 year over year compared to the 2022 limits. (When combined and maxed, you would have been investing $26,500 in 2022, and $29,000 in 2023). Stay with us, this is where the numbers get big!

This may not sound like a huge difference, but we encourage you to think about this long term. Maxing out your IRA and 401(K) to the 2023 limits compared to the 2022 limits (meaning an additional $2,500 dollars invested year over year) for 30 years, growing at a conservative 8%, would result in an additional $283,208!

Let’s take this a step further. Lets say you are an individual who is 35 years old when you begin maxing out your 401(k) and IRA. At age 50, you could take advantage of the catch-up contribution, and invest another $1,000 yearly. Again, assuming a 8% return for the remaining 15 years, that’s an additional $30,324 for a grand total of $560,440. That’s $313,532 more than if you were maxing out based on the 2022 limits.

Talk to your advisor today to make sure you are taking full advantage of these new laws!

*This hypothetical (like any investment, involves a chance of loss) assumes an 8% return throughout the life of the investment, and that the investor is 35 years old at start of investment and takes advantage of catch up contributions at age 50.

Find An Advisor.

work-optional

Visit Office Page >Reno, NV

Visit Office Page >Scottsdale, AZ

Visit Office Page >Larson Houston Branch

Visit Office Page >

Cottleville

Visit Office Page >Knoxville

Visit Office Page >Shreveport, LA

Visit Office Page >Fulton, MD

Visit Office Page >Brookfield, WI

Visit Office Page >Colorado Springs

Visit Office Page >Dallas, TX

Visit Office Page >San Diego, CA

Visit Office Page >Colorado

Visit Office Page >

Oakmont Financial

Visit Office Page >Denver, CO

Visit Office Page >Minneapolis West

Visit Office Page >

St. Charles

Visit Office Page >

Intrua Amarillo

Visit Office Page >

Intrua Dallas

Visit Office Page >

Intrua Wichita Falls

Visit Office Page >

T.A. Ohlms

Visit Office Page >

Rochester

Visit Office Page >

Omaha

Visit Office Page >

Minneapolis North

Visit Office Page >

Indianapolis

Visit Office Page >

Larson Capital Management

Visit Office Page >

Lakeland

Visit Office Page >

Kansas City

Visit Office Page >

Jacksonville

Visit Office Page >

Intrua Headquarters

Visit Office Page >

St. Louis Headquarters

Visit Office Page >

Great Lakes Regional Headquarters

Visit Office Page >

Fort Wayne

Visit Office Page >

Raleigh-Durham

Visit Office Page >

Waterloo Office

Visit Office Page >

Coconut Creek

Visit Office Page >

Chicago

Visit Office Page >

Filter By Office

Explore Industry Headlines

Stay up-to-date on the latest stories affecting the financial sector and your investments.