Our Leadership Team

Our Leadership Team

Find An Advisor

Find An Advisor

Our Platform

Our Platform

Advisory

Advisory

Alternatives

Alternatives

Insurance

Insurance

Specialized Services

Specialized Services

Individual Investors

Individual Investors

Retirees

Retirees

Business Owners

Business Owners

Family Offices & Institutions

Family Offices & Institutions

Doctors

Doctors

Tenants

Tenants

Accountants

Accountants

RIA / Advisor Firms

RIA / Advisor Firms

Tax Planning

Your January Tax Questions Answered

Posted on January 7, 2026

What to Expect (and What to Watch) in 2026

January has a way of arriving with fresh calendars, renewed motivation…and tax questions. If you’re wondering when your tax documents will arrive (or what’s changing for the year ahead) you’re not alone.

Below, we answer the most common tax-season questions we hear each year. We also share a few key 2026 planning updates which are worth keeping in mind as you look ahead.

Tax Document FAQs: What Arrives and When

What is a 1099 and Who Receives One?

1099 forms are used to report income you received that didn’t come from an employer. In other words, if income doesn’t show up on a W-2, it often shows up on a 1099. These forms report things like investment income (interest, dividends, and sale proceeds), retirement or annuity distributions, freelance or contract pay, certain government payments, and other non-wage income. The key thing to know: 1099s are informational. They summarize income paid to you during the year and are sent to both you and the IRS so that income can be properly reported on your tax return.

When will my 1099s be available?

Most 1099s are released in waves, not all at once.

- Schwab accounts: 1099s are typically available between late January and late February. Accounts with mutual funds, ETFs, or REITs, however, often receive forms later to avoid corrections from reclassified income. The most efficient way to access your tax documents is through their online portal. Use your Schwab Alliance login credentials to access your personal documents as soon as they are published.

- Fidelity accounts: if you have accounts with Fidelity, those 1099s are generally available between late January and mid-March. Timing depends on the specific form type and the complexity of your investments. Forms are often issued in staggered groups to ensure accuracy and avoid sending corrected statements later. Check the specific availability date for your forms by logging into your Fidelity account and navigating to the Tax Forms section.

What is Form 5498 and When Will it be Available?

Form 5498 reports IRA contributions and is sent directly to the IRS. It is not required to file your tax return. This is why it typically becomes available later in the year, usually after the April filing deadline. Form 5498 is simply an informational document to verify that you are staying within your contribution limits.

When will K-1s be available?

If you have investments with Larson Capital Management, K-1s are issued once all fund information is finalized. This often occurs close to the tax filing deadline. If you’re expecting a K-1, filing a short extension is common and often advisable. You’ll receive an email notification once K-1s are ready, and you can monitor their status through the Larson Capital Management investor portal.

Why Timing Matters More Than Ever

Understanding when documents arrive helps avoid unnecessary stress while also creating opportunity for smarter conversations. Filing later doesn’t mean procrastinating; it often means waiting for accurate information, so decisions aren’t rushed or reversed later.

That same mindset applies to tax planning for the year ahead.

Key 2026 Tax Updates to Know

As tax documents roll in, it’s helpful to understand what’s changed, and what hasn’t, for 2026.

- Tax brackets and standard deductions have increased: the federal tax bracket structure remains the same, but income thresholds rose due to inflation. This helps reduce “bracket creep,” meaning more income may be taxed at lower rates. The standard deduction also increased again. This allows more income to be shielded from federal tax, which can be impactful for retirees and those who don’t itemize.

- Additional benefits for those age 65 and up: in addition to existing age-based deductions, new provisions allow older taxpayers to claim a larger total standard deduction in 2026. For many households, this can reduce how much retirement income is taxable. This reinforces the importance of coordinating withdrawals, Roth strategies, and charitable giving.

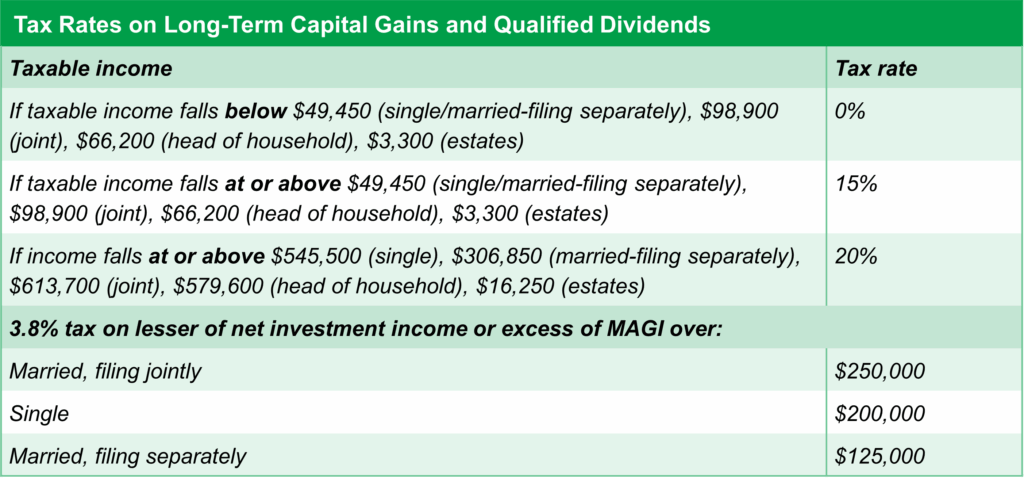

- Capital gains thresholds moved up: long-term capital gains rates remain at 0%, 15%, and 20%, but the income thresholds determining which rate applies increased. This creates potential opportunities around gain realization, especially when coordinated with other income sources.

Source: IRS

- Retirement contribution limits increased: 401(k) and similar plan limits rose again, with higher catch-up contributions available, especially for individuals ages 60–63. These final working years can be powerful for boosting long-term savings when contributions are planned intentionally.

- Estate and gifting rules remain favorable: the lifetime estate and gift tax exemption increased to $15 million per individual, while the annual gift exclusion rose to $19,000. These higher thresholds preserve flexibility for long-term legacy and gifting strategies.

A Helpful Next Step

As tax documents arrive and questions naturally pop up, remember you don’t have to sort through the details on your own. If something looks unfamiliar or sparks a bigger “Should we talk about this?” moment, that’s exactly what your advisor is here for. A quick conversation can help confirm you’re on track, and to help ensure this year’s tax decisions align with your broader financial plan.

Tax season doesn’t have to feel reactive. With the right timing and conversations, it can be a thoughtful reset that sets the tone for the year ahead.